You want to get ahead in life, right? Well, let me tell you, understanding the world of loans is crucial. Whether you’re looking to buy a new car, start a business, or purchase a home, knowing the ins and outs of different types of loans can make all the difference. From student loans to personal loans, mortgages to payday loans, each type has its own set of pros and cons. It’s time for you to take control of your financial future and make informed decisions about borrowing money. Trust me, you don’t want to be caught off guard when it comes to interest rates or repayment terms. So, buckle up, because we’re diving deep into the world of loans.

Key Takeaways:

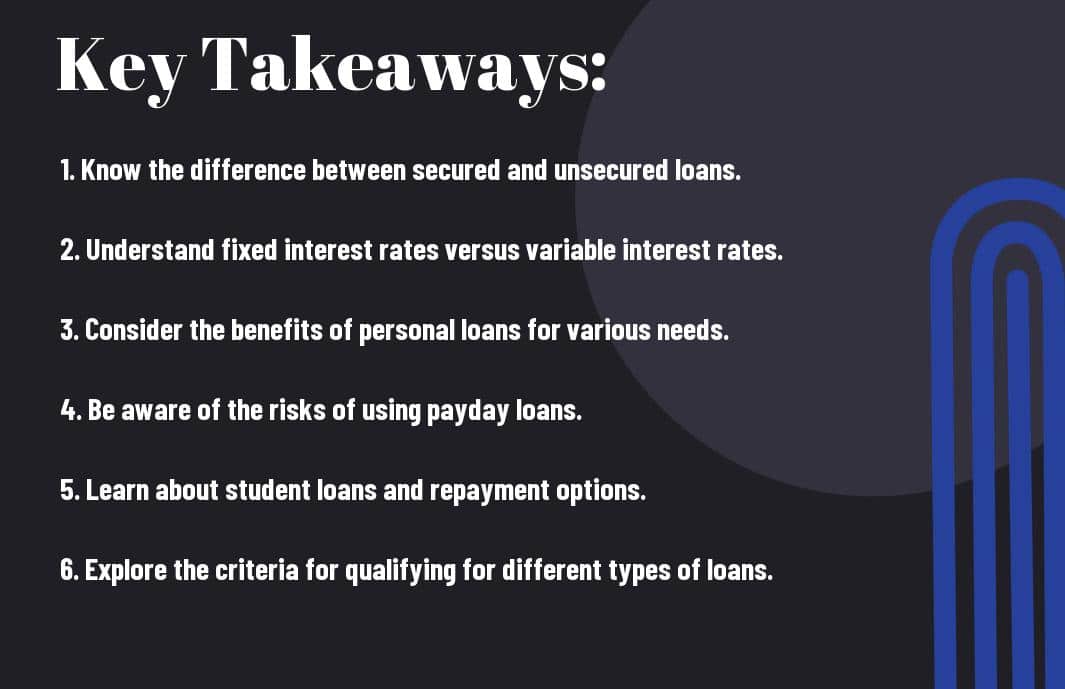

- Understand your needs: Before taking out a loan, make sure you understand your financial needs and choose the right type of loan that fits your specific situation.

- Research different types of loans: There are various types of loans available such as personal loans, student loans, mortgage loans, and more. Research each type to find out which one best suits your needs.

- Compare interest rates and terms: Different loans come with different interest rates and repayment terms. Compare these factors across different loan options to ensure you’re getting the best deal possible.

Unwrapping Personal Loans: Not Your Grandma’s Gift Money

Now, personal loans are a popular financial tool for many individuals looking to fund various expenses like home renovations, medical bills, or even starting a business. They are not just your grandma’s gift money anymore. Personal loans come in various shapes and sizes, each with its own set of terms, interest rates, and conditions.

Secured vs. Unsecured: What’s The Collateral Damage?

With personal loans, you’ll often come across the terms “secured” and “unsecured.” A secured personal loan requires collateral, such as your car or home, to back the loan amount. On the other hand, an unsecured personal loan does not require any collateral and is based solely on your creditworthiness. While secured loans may offer lower interest rates, they pose a higher risk of losing your assets if you default on the loan.

Navigating Interest Rates and Terms Like a Pro

Damage: This is where things can get tricky. When comparing personal loans, pay attention to the interest rates and terms offered by different lenders. Interest rates can greatly impact the total cost of your loan, so be sure to shop around for the best rate. Additionally, the loan terms, such as repayment period and any hidden fees, can significantly affect your overall financial health. Be sure to read the fine print and understand all the terms before signing on the dotted line.

Crushing It with Commercial Loans: Fuel for Your Business Fire

Once again, welcome back to my blog post on The Ultimate Guide to Loans – Everything You Need to Know. Today, we’re submerging into the world of commercial loans and how they can be the fuel your business needs to take things to the next level.

Understanding the Business Loan Jungle

Fuel your business growth with the right business loan! Navigating the business loan jungle can be tricky, but with the right knowledge and guidance, you can secure the funds you need to expand your operations, invest in new opportunities, or bridge cash flow gaps. Make sure to research different loan options, understand the terms and conditions, and choose the one that best fits your business needs. Do not forget, knowledge is power in the business loan jungle!

Mastering the Art of Repayment and Loan Covenants

Business, business, business! With respect to repayment and loan covenants, it’s vital to stay on top of your financial obligations. Do not forget, missing payments or violating loan covenants can have serious consequences for your business, including penalties, higher interest rates, or even default. Master the art of repayment by creating a solid financial plan, tracking your cash flow, and communicating openly with your lender to avoid any pitfalls. Stay ahead of the game and crush your loan repayments like a boss!

Home Loans: Building Your Dream Pad

Many people dream of owning their own home, where they can create a space that truly reflects their style and personality. However, buying a home is a significant financial investment that often requires taking out a loan. Understanding the different types of home loans available can help you make informed decisions and choose the option that best suits your needs and financial situation.

Mortgages Made Simple: Fixed Rate vs. Adjustable

Mortgages can be overwhelming, but they don’t have to be. Concerning choosing between a fixed-rate and adjustable-rate mortgage, the key difference lies in the interest rate. A fixed-rate mortgage offers the stability of a consistent interest rate over the life of the loan, making it easier to budget. An adjustable-rate mortgage, on the other hand, typically starts with a lower interest rate that can fluctuate with market conditions, potentially leading to lower payments initially but also posing the risk of higher payments in the future.

Refinancing: The How and Why to Redo Your Loan

Building your dream pad isn’t just about finding the right home loan – it’s also about knowing when to refinance. Refinancing your loan involves replacing your current mortgage with a new one, typically to take advantage of better terms, such as a lower interest rate or shorter repayment period. Refinancing can help you save money in the long run, but it’s vital to weigh the costs and benefits before making the decision.

Specialized Loans: The A-Z of Niche Borrowing

Getting Schooled on Student Loans

All right, everyone, let’s dig into the world of student loans. These loans are specifically designed to help you fund your education and cover everything from tuition to textbooks. Any student can apply for these loans, but keep in mind that they need to be paid back with interest once you graduate. Make sure to explore all the options available, including federal and private loans, and choose the one that works best for you.

Green Loans and Others: Financing Your Eco-Friendly Projects

Now, let’s talk about financing your eco-friendly projects with special green loans. Whether you’re looking to install solar panels, upgrade to energy-efficient appliances, or make your home more sustainable, there are Projects loans available to support your green initiatives. These loans often come with lower interest rates and flexible terms, making them a smart choice for environmentally conscious borrowers.

Borrowing money for your eco-friendly projects can not only help you reduce your carbon footprint but also save you money in the long run. By investing in green upgrades, you can increase the value of your property and lower your utility bills. Just remember to do your research, compare loan options, and choose a reputable lender to avoid any pitfalls in the process.

To wrap up

Understanding different types of loans is important for making informed financial decisions. Whether you need a personal loan, mortgage, auto loan, or student loan, knowing the differences between these options can help you choose the right one for your needs. Remember to compare interest rates, terms, and fees before signing any loan agreement. By staying informed and making smart choices, you can take control of your finances and build a solid financial foundation for the future. Keep hustling and making those savvy money moves!

FAQ

Q: What is a personal loan?

A: A personal loan is a type of loan that allows you to borrow a fixed amount of money which you repay over a set period of time with interest.

Q: How does a secured loan differ from an unsecured loan?

A: A secured loan requires collateral, such as your car or house, to secure the loan, while an unsecured loan does not require any collateral.

Q: What is the difference between a fixed-rate loan and a variable-rate loan?

A: A fixed-rate loan has an interest rate that remains the same throughout the life of the loan, while a variable-rate loan has an interest rate that can change periodically.

Q: How does a debt consolidation loan work?

A: A debt consolidation loan combines multiple debts into one single loan with a lower interest rate, making it easier to manage and pay off debt.

Q: What is a payday loan?

A: A payday loan is a short-term, high-interest loan that is typically due on your next payday. It is important to use payday loans responsibly to avoid falling into a cycle of debt.

Q: How does a student loan differ from other types of loans?

A: A student loan is specifically designed to help students pay for higher education. They usually have lower interest rates and flexible repayment options.

Q: What are some common reasons to take out a personal loan?

A: Common reasons to take out a personal loan include consolidating debt, paying for unexpected expenses, making home improvements, or funding a large purchase.